How Much House Can I Buy With My Paycheque?

One of the most common questions buyers ask is: How much house can I actually afford?

The short answer: it depends on your income, debts, down payment, where you buy and what you buy.

The longer (and more helpful) answer is below - translated into plain English, with real-world examples for Kitchener-Waterloo, Cambridge, and Guelph.

First, let’s decode the “rules” - lenders use two main guidelines when deciding how much they’ll lend you:

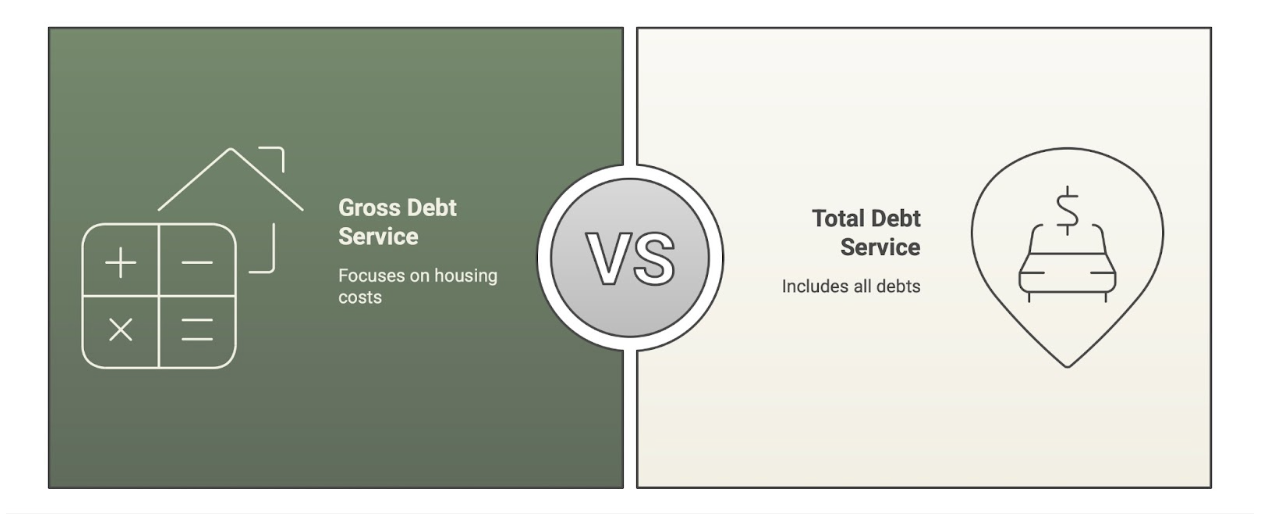

Gross Debt Service (GDS)

This is how much of your monthly income can go toward housing costs:

Mortgage payment

Property taxes

Heating

Condo fees (if applicable)

In simple terms: housing should usually stay under ~35% of your gross income.

Total Debt Service (TDS)

This includes everything:

Housing costs plus

Student loans

Car payments

Credit cards / lines of credit

Translation: all debts combined should usually stay under ~42% of income.

These ratios are tested using today’s typical mortgage rates, not the lowest rate advertised - a built-in buffer to make sure you can still afford your home if rates change.

Example 1: New Grad Buyer

Income: $45,000–$65,000

Down Payment: Minimum (5% on first $500k, 10% on the remainder)

Debt Assumptions: Student loan, no car payment

What this looks like in real life -

After accounting for student loan payments and today’s typical rates, most new grads fall into a purchase range of approximately: $350,000 – $450,000

Where this can work locally -

Kitchener-Waterloo: Entry-level condos

Cambridge: Older condos or smaller townhomes in select pockets

Guelph: Primarily condos; inventory is tighter at this level

At this stage, flexibility on location and property type is key.

Example 2: Solo Buyer

Income: $75,000–$95,000

Down Payment: Minimum first-time buyer structure

Debt Assumptions:

Modest car payment

Realistic credit card balance

What this looks like in real life -

With manageable consumer debt, many solo buyers land around: $500,000 – $625,000

How location changes your options -

Kitchener-Waterloo: Newer condos, stacked townhomes

Cambridge: Townhomes and select entry-level freeholds

Guelph: Condos or smaller townhomes

This is where city choice really matters - the same budget can buy very different homes depending on where you focus.

Example 3: Couple Buying Together

Household Income: $140,000–$180,000

Down Payment: Minimum first-time buyer structure

Debt Assumptions:

One student loan

One credit card payment

Two modest car payments

What this looks like in real life -

Even with mixed debts, dual incomes create flexibility. Many couples fall into a range of: $700,000 – $900,000

How far that budget goes -

Kitchener-Waterloo: Townhomes and some detached homes

Cambridge: Detached homes and newer developments

Guelph: Townhomes or older detached homes (pricing tends to be tighter)

This is where buyers often choose location based on lifestyle, commute, and long-term plans rather than “can we qualify?”

Why City Choice Matters More Than Buyers Expect

A townhome priced at $650,000 in Cambridge might cost:

More in parts of Kitchener-Waterloo

Significantly more in Guelph

Affordability isn’t just about income - it’s about matching your budget to the right market.

The Bottom Line

Your paycheque doesn’t decide your budget alone — your debts, down payment, and city choice all matter just as much.

That’s why two buyers earning the same income can qualify for very different homes.

Thinking About Buying And Want Real Numbers?

The Bunker Realty team helps buyers run personalized affordability scenarios and match them to the right neighbourhoods - before you fall in love with a home that doesn’t fit the budget.

Reach out anytime to start with clarity instead of guesswork.

—

Disclaimer: The price ranges and examples above are for educational purposes only. Individual affordability, mortgage approvals, and purchase prices vary based on lender guidelines, credit history, interest rates, down payment sources, and other financial factors. All mortgage approvals are subject to lender review and conditions.